.png)

.png)

The composite indicator that measures the trends in gold, crude oil, and yields on the 10 year Treasury has moderated significantly. See figure 1 a weekly chart of the S&P500 with the indicator in the lower panel.

Monday, November 30, 2009

Saturday, November 28, 2009

Investor Sentiment: Waiting For The "R" Word

As expected, last week's holiday infested market action provided little clarity. The sentiment picture remains relatively unchanged. Nonetheless, there was a market moving event, and the "default in Dubai" will likely leave investors with one of two conclusions: 1) coordinated efforts by central bankers to re-liquify the world economy are likely to continue as bad news means good news --the proverbial punch bowl will be with us for awhile; or 2) the house of cards -otherwise known as the recovery - is beginning to look a little wobbly; central bankers, no matter how hard they try, are unable to fight the forces of deleveraging. This contagion just won't go away so easily.

The "default in Dubai" is interesting as this now becomes a test of central banker resolve to keep the balls in the air. The US equity rally has been looking a little weak over the past two months and this could be the scare that moves a lot of money to the sidelines. Where there is one cockroach, there is bound to be others. But I suspect this will be passed off as nothing more than a hiccup, and will unlikely derail the bullish fervor. The only thing that can do that is lower prices.

What the "default in Dubai" says is that risks are mounting. This is not "wall of worry" nonsense. This is just common sense after a 60% plus move in the S&P500 over 8 months. Common sense often doesn't work in the markets, but fundamentals, valuations, technicals, and sentiment do not support higher prices. Dollar devaluation and ongoing Federal Reserve complacency are reasons why stocks can go higher, but this will have its limits I suspect. It is not a reason why I would be a buyer of equities with the expectation that this represents a golden buying opportunity. I am just waiting for someone on CNBC to utter the "R" word: resilient. When you hear that word, make sure you run for the exits.

From my data driven perspective, I will state what I said last week and for many weeks before that:

"The major equity indices are in a topping process. This implies a trading range at best. There is risk of a down draft as markets "fueled" by the proverbial "liquidity" are prone to quick sell offs. The outlier trade is a market blow off or a spike in prices, and I do not rule this possibility out because of the ongoing downtrend in the Dollar Index. It is possible but it is not the high odds play. This is not the market environment that will take you from here to there."

The "Dumb Money" indicator, which is shown in figure 1, looks for extremes in the data from 4 different groups of investors who historically have been wrong on the market: 1) Investor Intelligence; 2) Market Vane; 3) American Association of Individual Investors; and 4) the put call ratio. The "Dumb Money" indicator shows that investors are extremely bullish.

Figure 1. "Dumb Money" Indicator/ weekly

The "Smart Money" indicator is shown in figure 2. The "smart money" indicator is a composite of the following data: 1) public to specialist short ratio; 2) specialist short to total short ratio; 3) SP100 option traders. The Smart Money indicator is neutral.

Figure 2. "Smart Money" Indicator/ weekly

Figure 3 is a weekly chart of the S&P500 with the InsiderScore "entire market" value in the lower panel. From the InsiderScore weekly report we get the following two insights: 1) S&P500 weekly score falls to 30 month low; 2) buyers are not showing the type of conviction that sellers are.

Figure 3. InsiderScore Entire Market/ weekly

Figure 4 is a daily chart of the S&P500 with the amount of assets in the Rydex Money Market Fund in the lower panel. When the money market fund is flush with cash, one can assume that the Rydex timers (like market participants in general) are fearful of market losses. From a contrarian perspective, these are good buying opportunities. When the amount of assets are low (like now), these market timers are all in; one should be on the lookout for market tops. There is little buying power left. As of Friday's close, assets in the money market fund are off the lowest of the year seen in the previous week.

Figure 4. Rydex Money Market/ daily

Friday, November 27, 2009

Utility ETF Set To Breakout

In his most recent commentary, PIMCO's Bill Gross provides his rationale to invest in utility stocks.

Gross suggests that the Federal Reserve will remain accommodative for a very long time:

"Raise interest rates with 15 million jobless and 25 million part-time working Americans? All because gold is above $1,100? You must be joking or smoking – something. We will need another 12 months of 4-5% nominal GDP growth before Bernanke and company dare lift their heads out of the 0% foxhole – mini-bubbles or not."

Why is the Fed doing this?:

"The Fed is trying to reflate the U.S. economy. The process of reflation involves lowering short-term rates to such a painful level that investors are forced or enticed to term out their short-term cash into higher-risk bonds or stocks."

And there is the rub. There is no safe place to park your cash money. As Gross asks with a series of questions:

"OK, so where does that leave you, the individual investor, the small saver who is paying the price of the .01%? Damned if you do, damned if you don’t. Do you buy the investment grade bond market with its average yield of 3.75% (less than 3% after upfront fees and annual expenses at most run-of-the-mill bond funds)? Do you buy high yield bonds at 8% and assume the risk of default bullets whizzing at you? Or 2% yielding stocks that have already appreciated 65% from the recent bottom, which according to some estimates are now well above their long-term PE average on a cyclically adjusted basis?"

So Gross concludes that utilities with their high yields, fair performance year to date, and likely in line growth with the US economy would be a good place for his money:

"Why not just buy utilities if that’s what the future American capitalistic model is likely to resemble. Pricewise, they’re only halfway between their 2007 peaks and 2008 lows – 25% off the top, 25% from the bottom. Their growth in earnings should mimic the U.S. economy as they always have, and most importantly they yield 5-6% not .01%! In a low growth environment, it seems to me that a company’s stock should yield more than its less risky debt, and many utilities provide just that opportunity. Utilities and even quasi-utility telecommunication companies now yield between 5 and 6%, whereas their 10- and 30-year bonds yield less and at a higher tax rate to you the investor."

Now let's take a look at the S&P Select Utilities Spider Fund (symbol: XLU). See figure 1 a weekly chart. The indicator in the lower panel measures the distance between the upper and lower Bollinger Bands; this value is wrapped in trading bands that looks for statistically significant extremes. The difference between the upper and lower Bollinger Bands is a measure of volatility. Prior to (up or down) breakouts, prices will typically move in a range as buyers and seller become in balance. Price range or volatility will contract. This is what the indicator measures. As prices contract, the bands narrow. When prices breakout (to the upside for example) buyers overwhelm the sellers, price and volatility expand. The Bollinger Bands widen. Viola, the breakout!

Figure 1. XLU/ weekly

So if I were to define a "breakout" this is how I would do it: 1) price must be consolidating to a statistically significant degree and with the XLU, this is the case as the indicator is below the lower trading band; 2) the trigger to enter the trade would be a weekly close over the trend line formed by two down sloping pivot points, and with the XLU, this appears to be the case as the week comes to a close. This would be above 29.57 on XLU. A reasonable stop loss, which would indicate that this trade is a failure, would be a weekly close below the most recent pivot low point (blue up arrows) at 28.94.

The width of the base (or prior trading range) is about 6 XLU points. Therefore, a reasonable target for XLU is 36 (i.e., breakout point at 30 +6 point base= 36). This also happens to correspond with its breakdown point seen in September, 2008.

Wednesday, November 25, 2009

Bond ETF Under Accumulation

As long as we are talking Treasury yields today, I thought I would take a look at two charts that suggest that longer term Treasury yields are headed lower, and this should be a tradeable move, which means you won't have to "thread the needle" to make some money. In other words, I cannot imagine it being secular in the sense of lasting months, but several weeks would seem likely.

Before looking at the charts, I want to point you to two recent articles that I wrote on this topic:

"The Technical Take: Are Treasury Yields Headed Lower?" (November 16, 2009)

"Bond Sentiment: Very Interesting" (November 20, 2009)

Figure 1 is a weekly chart of the yield on the 10 year Treasury. It looks like yields will close the week below the down sloping trend line (prior breakout point) and the 40 week moving average. The implications of a failed breakout and a close below the 40 week moving average suggests much lower yields. In addition, 10 year Treasury yields will remain below the key monthly pivot at 3.432, which we have been talking about for 10 months now, for 4 months running.

Figure 1. 10 year Treasury Yield/ monthly

Conversely, we can look at figure 2, which is a daily chart of the i-Shares Lehman 7-10 year Treasury Bond Fund (symbol: IEF). As yields move lower, this fund or ETF moves higher. Volume bars are in the middle panel and the on balance volume indicator (with 40 day moving average) is in the lower panel. This ETF is under accumulation. The on balance volume indicator is making new highs and leading price higher. Price is breaking above the 200 day moving average today albeit on below average volume.

Figure 2. IEF/ daily

In light of the known divergence between the Treasury market and equities, today's developments are worth noting. With a stock market looking somewhat toppy and yields falling, I am inclined to interpret falling yields as economic weakness. Over the past 8 months, economic weakness has meant more economic stimulus and of course, Wall Street loves that stimulus. But now we have an equity market that has gained 60% plus in 8 months, and despite this fact, there is still much uncertainty regarding the recovery.

I guess there is a limit to everything (including the stimulus) and we shall soon find out.

Just Catching On

Today must be MarketWatch day.

Mark Hulbert has a very good article on the divergence seen between Treasury bill yields and equities. In essence, T-bill yields are at the same level they were during the Lehman Brothers meltdown, when the fate of the world was at risk due to the possibility of a financial meltdown in the U.S.

I made a similar observation (with longer dated Treasury bonds) in an article written on August 26, 2009 entitled "Long Term Treasury Yields: Someone Is Going To Be Wrong". Once again, it was the divergence between Treasury yields, which were headed lower, and stocks, which were headed higher, that caught my attention. After all, stocks were forecasting economic strength and lower yields would seem to suggest economic weakness. Both markets cannot be right. Or can they?

Hulbert does ask the right question:

"But why should rates be just as low today? After all, it would certainly appear as though today's economic and financial conditions couldn't be more different."

"Take the stock market, for example, which is coming off the strongest eight-month rally in decades. The S&P 500 index (SPX 1,108, +2.53, +0.23%), in fact, is up some 66% since the March 9 market low. Benchmarks of secondary stocks have performed even better, with the Wilshire US Micro-Cap Index up nearly 100% since the bear market's lows."

Hulbert goes on to answer his own question with a question:

This behavior would seem to indicate that investors have become less and less worried about economic and financial risks. Yet, if that were the case, why would T-Bill yields be back down at levels suggesting that those risks are just as bad today as they were at the heights of financial panic one year ago?

Let's be clear, Hulbert doesn't have the answer and neither does famed newsletter writer, Richard Russell, who calls the situation "the mysterious disconnect". However, I do like Hulbert's choice of words that one of these two markets is "out of touch of with reality" and that given the vastness of both markets, it is very "sobering" to ponder that a lot of people are going to be wrong.

I Am So Breathless

This image is from MarketWatch just prior to today's open.

When I see stuff like this, I am just left breathless as I am struck with fear that the stock train has left the station without me. My goodness after a 60% plus run in the market, stocks are "accelerating" higher. I better jump on board!!!

How about the "before the bell countdown"? I better sync my wristwatch to the exact second so I don't miss a single tick.

Or how about the cry to take your "battle stations"? Such imagery and such foolishness. I can just see myself strapped into my chair in front of the computer with my Army helmet on ready to go. "Battle stations. Are you ready? The market opens in 26 minutes and 23 seconds."

I don't know why anyone would find any of this useful. It perpetuates the image that the stock market is nothing more than a casino that can be gamed on a consistent basis. I think this is particularly hard to do day in and day out. Get out the pom poms as we take one poorly constructed data point, put a positive spin to it, and hope that it juices the market.

Excuse my cynicism but I just wonder where is the value in such hysteria? It may be news but it is not newsworthy.

Monday, November 23, 2009

Thanksgiving Week Trading

In this week's comments on investor sentiment, I alluded to the positive seasonality seen in the stock markets during the week of Thanksgiving. Here is some compelling data.

This is a very nice table from Trader's Narrative showing how the S&P500 has performed over the last 20 years during the Thanksgiving holiday week. My thanks to Babak for allowing me to share this with my readers.

Table 1. S&P500 Performance/ Thanksgiving Week

While the table covers only 20 years, the article presents some numbers going back to 1950. In essence, the data supports the notion of an upside bias to the week, and in particular, the trading days around the actual Thanksgiving holiday are very positive. Sellers are not out in force, and buyers will push a low volume market higher.

Unfortunately, the good holiday vibe is short lived as the week after Thanksgiving week tends to be a little less bullish.

Sunday, November 22, 2009

Investor Sentiment: Happy Thanksgiving!

In this holiday shortened week, there won't be much to gleam from market action in the coming week.

Over the past couple of months, Mondays have been kind to the bulls. Wednesday will be light as traders ready for Turkey Day on Thursday. Friday is another snooze fest that seems to go to the bulls --why spoil a great American holiday?

Will this week be another repeat of the last two where the best gains are on Monday and then the market struggled all week long? It seems plausible. Stock sponsorship (i.e., volume) has been pathetic, and I can't see that improving this week either.

"The major equity indices are in a topping process. This implies a trading range at best. There is risk of a down draft as markets "fueled" by the proverbial "liquidity" are prone to quick sell offs. The outlier trade is a market blow off or a spike in prices, and I do not rule this possibility out because of the ongoing downtrend in the Dollar Index. It is possible but it is not the high odds play. This is not the market environment that will take you from here to there."

Have a Happy Thanksgiving!

The "Dumb Money" indicator, which is shown in figure 1, looks for extremes in the data from 4 different groups of investors who historically have been wrong on the market: 1) Investor Intelligence; 2) Market Vane; 3) American Association of Individual Investors; and 4) the put call ratio. The "Dumb Money" indicator shows that investors are extremely bullish.

Figure 1. "Dumb Money" Indicator/ weekly

The "Smart Money" indicator is shown in figure 2. The "smart money" indicator is a composite of the following data: 1) public to specialist short ratio; 2) specialist short to total short ratio; 3) SP100 option traders. The Smart Money indicator is neutral.

Figure 2. "Smart Money" Indicator/ weekly

Figure 3 is a weekly chart of the S&P500 with the InsiderScore "entire market" value in the lower panel. From the InsiderScore weekly report we get the following three insights: 1) after stripping out the buying in the financial sector from Regional Bank insiders, the "entire market" score was the second worst weekly score since June, 2007; 2) Technology and Basic Material were the driving forces of negative sentiment; 3) insider buying in the Regional Bank sector has been noteworthy and we highlighted this in the article: "The New World Of Investing".

Figure 4 is a daily chart of the S&P500 with the amount of assets in the Rydex Money Market Fund in the lower panel. When the money market fund is flush with cash, one can assume that the Rydex timers (like market participants in general) are fearful of market losses. From a contrarian perspective, these are good buying opportunities. When the amount of assets are low (like now), these market timers are all in; one should be on the lookout for market tops. There is little buying power left. As of Friday's close, assets in the money market fund remain very near their lowest levels since the rally began in March, 2009.

Figure 4. Rydex Money Market/ daily

Saturday, November 21, 2009

The Greats Of The Blues: Walter Horton

Harmonica player Walter Horton, better known as Big Walter, was born in Mississippi on April 6, 1917. He spent much of the 1930's and 1940's travelling and playing through the South, and his earliest known recording was in 1939. He arrived on the Chicago Blues scene in the early 1950's where he backed Muddy Waters and other Mississippi Delta Blues performers who had traveled north for a better life in the big city. In the 1960's, the white youth of America "discovered" this harmonica virtuoso, and in the 1970's, he toured the world and frequented the festival circuit. He died in 1981 of heart failure.

There is more that is not known about Big Walter than is known. He was said to be a quiet and shy man, who was also nicknamed "Mumbles" and "Shakey". Big Walter boasted that he taught Little Walter and the original Sonny Boy Williamson to play harmonica. Most Blues historians doubt this contention. What isn't contested is this: Big Walter was one of the most influential harmonica players in the history of the Blues. His tone or big sound is instantly recognizable. Nobody played the harmonica like Big Walter.

To read more about the life of Big Walter Horton, check out this link at Wikipedia.

Friday, November 20, 2009

Bond Sentiment: Very Interesting

I am definitely on board with the idea that longer dated Treasury yields are headed lower, and I am beginning to warm up to the idea that this could be meaningful, tradeable move.

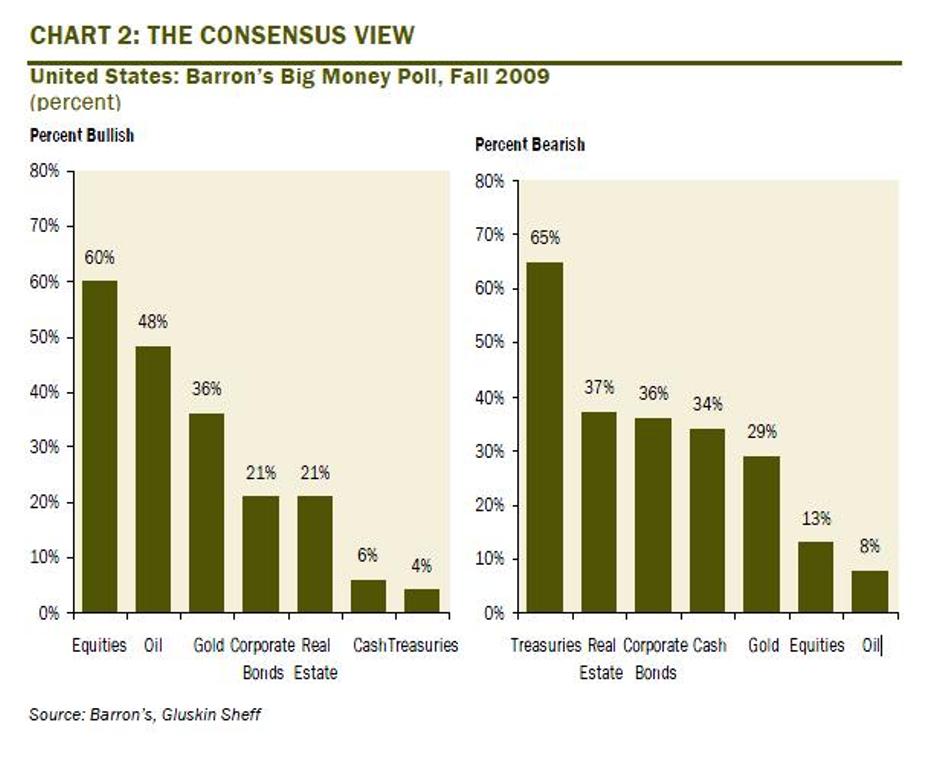

Now from the missives of David Rosenberg, we have the Barron's Big Money Poll from Fall, 2009. The most loved asset class: equities. As it turns out, Treasuries are the least loved and the most hated - winning both titles by a long shot. See figure 1.

Figure 1. Barron's Big Money Poll

Very interesting.

Rydex Market Timers: Persistence

The Rydex market timers remain persistent in their desire to buy the dip.

Figure 1 is a daily chart of the S&P500 with the amount of assets in the Rydex Money Market Fund in the lower panel. This value is now at its lowest point since the rally began in March, 2009.

Figure 1. S&P500 v. Rydex Money Market/ daily

Figure 2 is a daily chart of the S&P500 with the amount of assets in the Rydex bullish and leveraged funds versus the amount of assets in the leveraged and bearish funds. There is minimal change from yesterday.

Figure 2. Rydex Bullish and Leveraged v. Bearish and Leveraged/ daily

Thursday, November 19, 2009

Rydex Market Timers: At It Again

The Rydex market timers are buying the dip to an extreme degree.

Figure 1 is a daily chart of the S&P500 with the amount of assets in the Rydex Money Market Fund in the lower panel.

Figure 1. S&P500 v. Rydex Money Market/ daily

Figure 2 is a daily chart of the S&P500 with the amount of assets in the Rydex bullish and leveraged funds versus the amount of assets in the leveraged and bearish funds.

Figure 2. Rydex Bullish and Leveraged v. Bearish and Leveraged/ daily

Subscribe to:

Comments (Atom)

.png)